GenAI is also driving the e-discovery market. As a result, the methods, workflows and analysis procedures in the context of litigation, investigation, compliance, cyber, and regulatory are being questioned. From a business perspective, this presents a range of opportunities as well as challenges. What improvements in terms of insight, efficiency, quality, and usability can be achieved through GenAI-based approaches? Are GenAI-based work results equally reliable? What is the potential for cost savings in specific aspects of e-discovery? To answer these questions, a clear understanding of the current level of standardization and the characteristics of companies’ case portfolios is foundational.

In German-speaking countries (referred to as “D-A-CH”), the topics mentioned above are met by companies with very different levels of experience and maturity in data-driven investigation of facts. For this reason, Deloitte has, for the first time, collected a snapshot of e-discovery and the associated data management in German-speaking countries as part of a study in which more than 500 company representatives from various industries participated. This article provides early insights into selected topics of the survey, which will be published in early 2026.

Companies surveyed

German-speaking companies were surveyed, 51% of them in Germany, 25% from Austria and 24% from Switzerland. All major industries were taken into account, including banking, insurance and financial services, automotive, life science and healthcare, transport and logistics, as well as the public sector and public administration. The distribution of revenues ranges in clusters from less than €50 million to more than €3 billion. 89% of respondents in the companies are familiar with the term e-discovery. The feedback clearly shows that e-discovery has established itself as a specific and adapted instrument for dealing with fact-finding among German-speaking companies across all industries.

First results

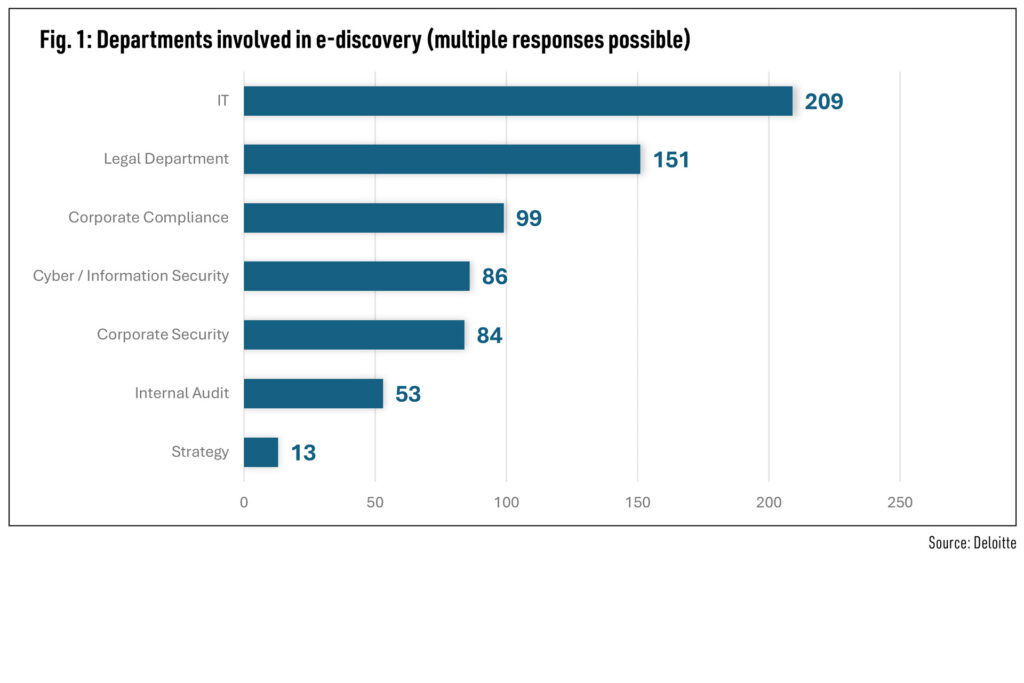

Participating departments

Traditionally, legal, corporate compliance and IT continue to be key departments for handling e-discovery cases. However, there is also clear relevance for other functional domains. The technologies and analytical methods of e-discovery have found their way into cyber/information security, corporate security and internal audit (fig. 1).

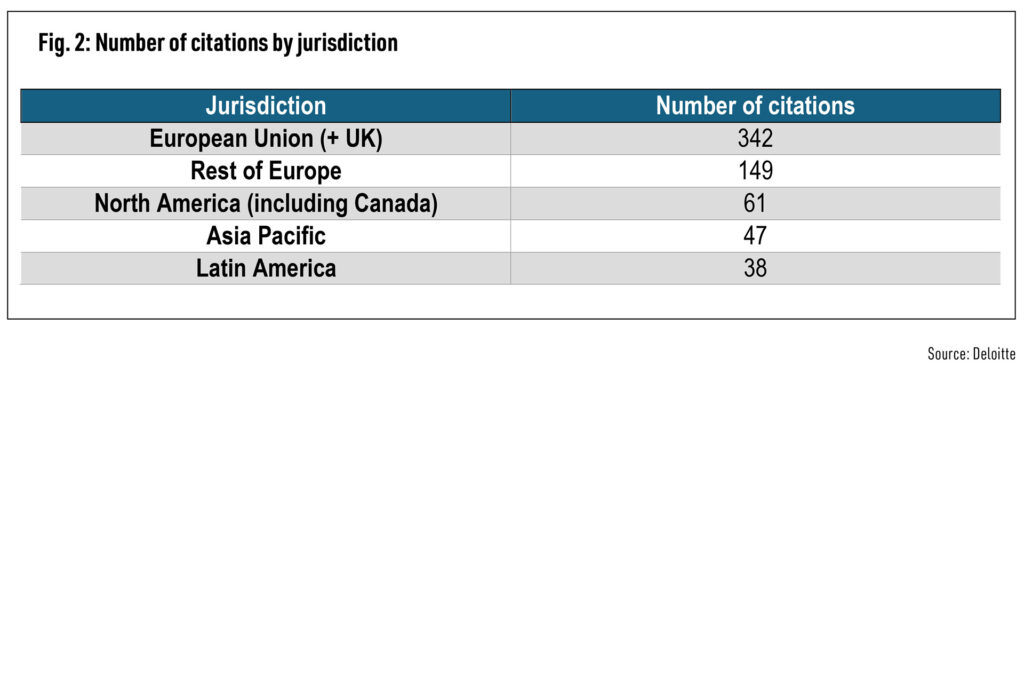

Jurisdictions

The case portfolio covers all jurisdictions, with multiple responses possible. The predominant jurisdiction typically has a decisive impact on the choice of e-discovery platform or software solution used to implement the EDRM process. The US market continues to dominate the range of e-discovery software solutions. In light of increasing geopolitical uncertainty, the analysis of the determining jurisdictions in the case portfolio can therefore be a relevant analysis in the context of software or technology procurement for one or the other company (fig. 2).

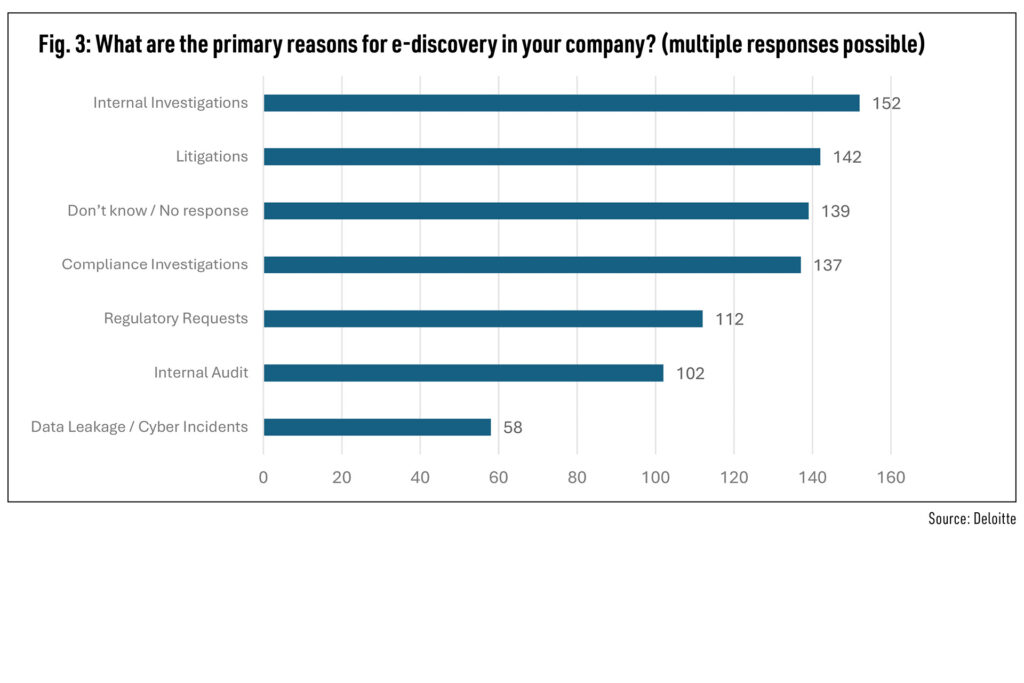

Primary triggers

The primary triggers of e-discovery include internal investigations, compliance violations, legal disputes, regulatory inquiries, audits, and data breaches or cyber incidents (fig. 3).

Case portfolio

62% of respondents reported having 1 to 10 discovery cases in the past five years. 20% reported 11-50 cases and only 3% reported more than 50 cases. Often fewer than 5 (19%) or 5-10 (22%) custodians are involved. However, 14% of the respondents also reported an average custodian count of 11-20 custodians and 4%, 21-50 custodians. Cases with more than 50 custodians are rare. 20% of respondents reported an average case duration of 1-3 months, 26% reported 3-6 months, and 13% reported 6-12 months. This means that the smaller cases, with a duration of 1-12 months, dominate the e-discovery portfolio of the companies surveyed. Only 3% of the companies surveyed stated an average case duration of more than 12 months, and 1% of more than three years.

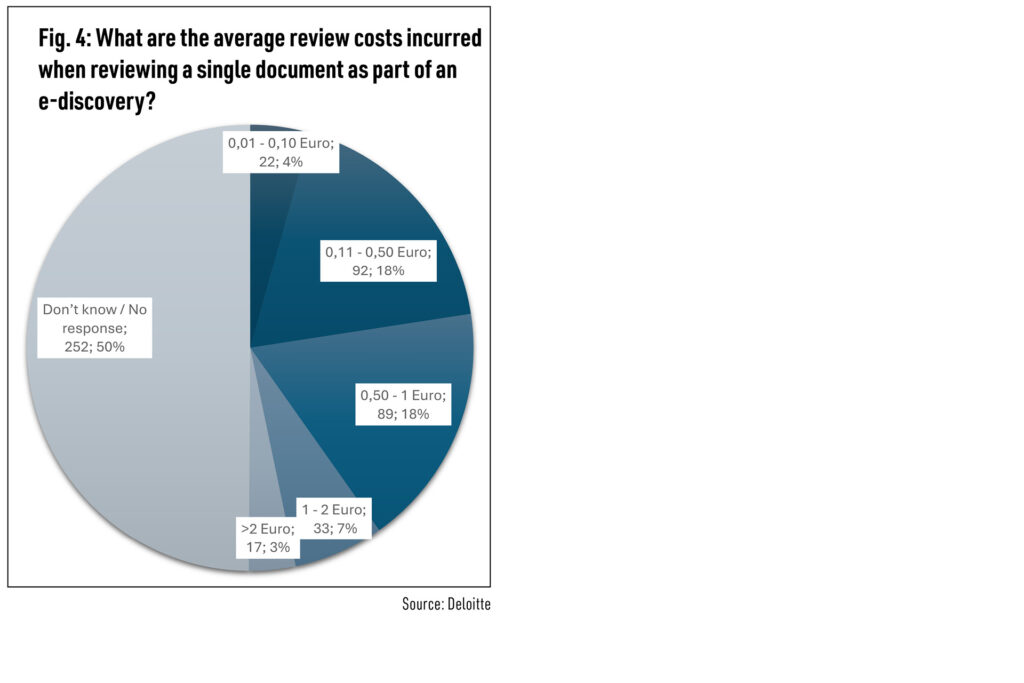

Cost

The average cost for a complete e-discovery is less than €3,000 per case. At 48%, almost half of the respondents reported average costs of €500-1,000, 25% reported €1,500-3,000 and 7% reported over €3,000.

The average review costs per document range from less than 10 cents to more than €2.

The costs are largely uniform both in terms of industry and revenue clusters. There is significant potential for cost reduction through automation, machine learning and generative AI. In the case of standardizable reviews, such as PII reviews or certain clearly definable confidential information, extensive automation of the review procedures is possible (Fig. 4).

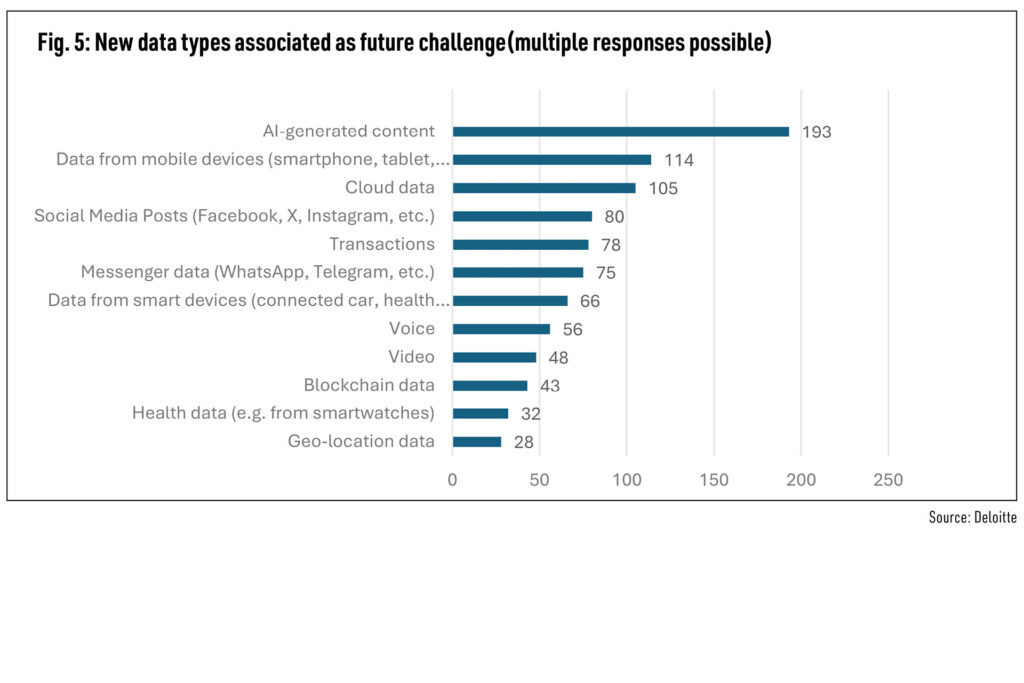

Challenges and risks

In the future, more and new types of data will need to be considered. Respondents associate the biggest challenges for e-discovery in the next few years with AI-generated content, data from mobile devices (smartphones, tablets, etc.), cloud data social media posts, and transactional data.

The risk associated with “Dark Data” (chart not displayed) now seems somewhat diminished. Perhaps it is often too vague to trigger a call for action considering a generally extensive list of mandatory tasks and corrective actions in e-discovery. In any case, Dark Data is not primarily associated with e-discovery risks. Respondents stated that the greatest concern with Dark Data is associated with data protection and compliance. A very clear picture emerges when it comes to the risk of storing data in the cloud. Almost two-thirds of respondents have few to no concerns about storing data in the cloud. Only 11% of those surveyed express concerns. Apparently, while handling data from the cloud is considered challenging, conducting e-discovery in the cloud is not (Fig. 5).

Outlook

This pre-read of the study already provides a snapshot of e-discovery in German-speaking (D-A-CH) countries. The case portfolios are homogeneous. Costs are clearly defined. They can be used as a basis for comparison with new GenAI scenarios. The number of departments for which e-discovery methods and technologies are relevant has increased. Answers to questions such as how standardized departments’ operations are, which competencies are required internally, and which can be outsourced, as well as many other insights and conclusions, will be presented in the complete survey.